New York hedge fund Elliott Management is best known for hardball tactics that have seen it take on governments and large corporations. But in the UK it has a different pitch: it wants to sell sushi, paperbacks, and now washing machines.

The famed activist investor is trying to buy electronics retailer Currys, adding to an already extensive portfolio of well-known components of the UK high street, including stakes in bookseller Waterstones, accessories retailer Claire’s and restaurant chain Wasabi.

Elliott has also backed credit investor Bantry Bay, which has loaned more than £400mn over the past 18 months to clothing companies Superdry and Matalan, as well as online fashion platform Asos.

The contrarian bets are spearheaded by Paul Best, a low-key 45-year-old, who in a two-decade investing career has managed to strike a series of winning deals in a sector that has claimed the scalps of many of his private equity peers.

They also highlight the increasingly creative approach that the $65bn hedge fund and private equity group is taking to make money, branching out further from the high-profile activist campaigns in listed companies that made its fearsome reputation.

Within Elliott, Best’s UK dealmaking is just a part of the firm’s growing private equity footprint. Its biggest deals and largest allocation are to the US market, where in the past two years it has partnered with other investors to buy software company Citrix for $16.5bn including debt, and television data ratings group Nielsen for $16bn.

But while the sums at stake in the UK may be small by Elliott’s standards, their success or failure may have outsized impact on the future of the high street.

Elliott and Best declined to comment.

Best, who has a first-class maths degree from the University of Cambridge, started his career with a stint in investment banking at Wall Street powerhouse Morgan Stanley.

A move to large US investment firm Warburg Pincus soon followed where he worked on an early deal that would bolster his standing as a consumer dealmaker: a £200mn investment in UK discount retailer Poundland that Warburg made in 2010 and where Best sat on the board.

The deal was well timed as consumers flocked to budget stores like Poundland in the aftermath of the financial crisis to cut back on their shopping bills.

The retailer’s revenues increased by 73 per cent and operating profit nearly doubled before Warburg took Poundland public in 2014, making Warburg at least three-and-a-half times its initial investment.

Best’s success boosted his career, with one adviser describing it as his “claim to fame.”

In 2016, Best led another Warburg high street bet when it bought a majority stake in fashion brand Reiss, in a deal valuing the business at more than £200mn.

It was another typical Best transaction: small, high-profile and nonconformist.

Elliott soon came calling. In 2017, the hedge fund was seeking to scale up in private equity, an asset class that had benefited from central banks keeping interest rates at near record lows.

Elliott had previously dabbled in UK retailers — including profiting, controversially, from the demise of electrical goods chain Comet. It also successfully invested in the video game chain Game Retail.

Best was hired in a new role to lead Elliott’s private equity push in Europe, where senior executives including Gordon Singer — the son of Elliott’s founder, Paul Singer — saw opportunities. Best was seen as a highly competent, safe pair of hands to seek out these investments.

“He’s just right for them,” said one person familiar with Elliott and Best. “They wanted a highly accomplished senior worker who will never challenge for the title.”

Within a year of joining, Best’s first opportunity came up.

The then-owner of bookshop chain Waterstones wanted to sell the business after nearly a decade of ownership. Elliott signed a deal in April 2018 to buy it for about £160mn.

The acquisition was a gamble on a sector that had seen Amazon and other online competitors cannibalise business. Best took the view that there was still a place in the market for a bookseller that offered a decent in-store experience.

The next year Elliott doubled down on this trend, buying US chain Barnes & Noble for $683mn.

Under Elliott’s ownership, Waterstones has added scores of stores and also acquired rivals Foyles and Blackwell’s, defying predictions that the internet and Amazon would kill off the bookshop.

Elliott has yet to take any money out of the bookshop chains, which are instead investing profits in a US expansion that will add more than 50 stores this year alone.

This shows the longer-term strategy behind Elliott’s ownership. Waterstones boss James Daunt has told the Financial Times that the public market “would be a very sensible place” for the bookseller, although those close to the situation say that a listing is unlikely to happen this year.

One executive who has worked with Best said Elliott was “looking where others aren’t”, adding that they did not think there was a “massive grand plan” underpinning the deals.

“Naturally they would look to get some value out of it but they don’t start at ‘what’s the value extraction?’” they added. “They would ask: ‘is it potentially under-explored, is there room to grow?’”

Last year, the firm weighed a bid for The Body Shop and was also in the running to take over Reiss. Elliott ended up passing on The Body Shop and was pipped by retailer Next, an existing shareholder, in buying Reiss.

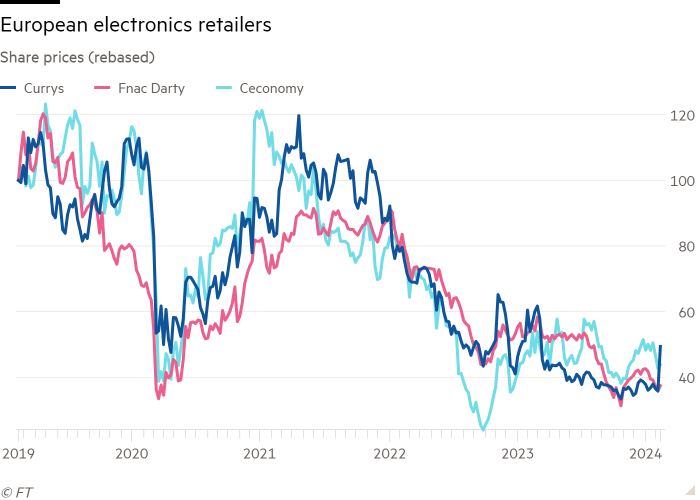

In February, the firm’s latest target became known: Currys, which had previously seen its stock plummet 65 per cent over the past five years.

Elliott has eyed the business as a possible acquisition target for several years, according to people familiar with the matter. However, the investment group’s initial two bids in February of 62p a share and then a revised offer of 67p last week were viewed as too low and rejected quickly by the company.

Analysts at Peel Hunt said the company’s board was unlikely to engage on anything “less than 80 pence”.

Currys’ market capitalisation of about £750mn could make it a tempting target for Elliott given that it appears to be trading at a discount to the sum of its various businesses.

The group’s electronics refurbishment division and its mobile businesses alone could be worth more than £1bn, analysts at Investec previously calculated.

Chinese ecommerce company JD.com has also emerged as a rival, saying in February that it was considering an offer.

Although Elliott’s fund structure allows it to hold assets indefinitely, whether Best’s bets on the British high street end up paying out for the firm will only be determined upon exit.

Until then, “the jury is out”, one Elliott backer said.

Additional reporting by Costas Mourselas in London

{kind=link}