You win some, you lose some. The London Stock Exchange has already suffered the departure of a number of stalwarts. European tour operator Tui is the latest to plot an exit. The LSE has also failed to woo others, including homegrown chip designer Arm.

But a new dawn beckons as government, regulators and capital markets participants once again strive to turn around the exchange’s fortunes. Kazakh carrier Air Astana has already swooped in as an early arrival.

This is, perhaps, not the company to win over naysayers. Kazakhstan’s national carrier hails from a land in which UK investors have been burnt in the past. Recall Kazakh miner Eurasian Natural Resources Corp, a one time-FTSE 100 member with ghastly governance, which ultimately delisted.

Of course, Air Astana is a different company. It was 49 per cent owned by BAE Systems (15 per cent post listing), and operates a fleet of 50 aircraft. Still, airlines are not the sector to set hearts beating. Funds raised were piddly even without being compared with Arm’s near $5bn.

The idea that reform is needed is the one consensus in the hullabaloo surrounding London’s financial markets. Proof is provided by the verbiage this has occasioned: Ron Kalifa, Jonathan Hill, Mark Austin and Douglas Flint are among the luminaries to steer government-commissioned reports.

One upcoming report, dubbed “The Capital Markets of Tomorrow”, aims to join the dots and layer more on top.

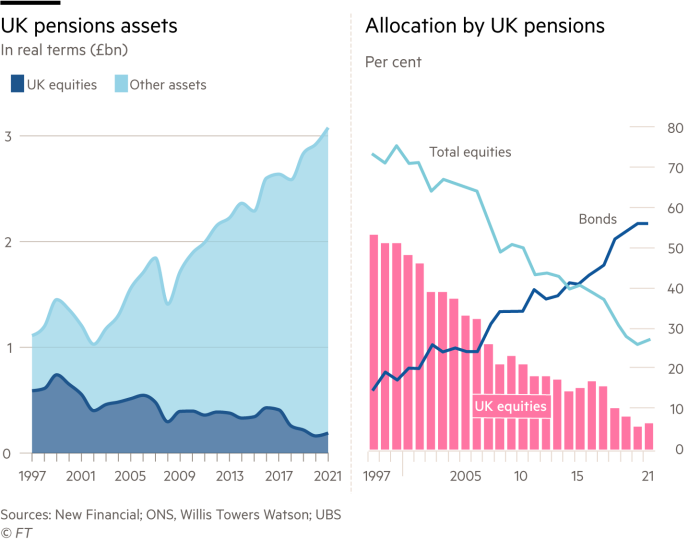

Still, it is hard to ignore the disjointed nature and vested interests that pit parties against each other. The underlying issue is that, even as assets in UK pensions have grown, an ever-smaller proportion of them is being invested in UK equities. Lighter touch regulation and a deepening of investment choices will attract more candidates, but raise risk factors.

Disclosure-based regimes — in which investors have all the facts at the click of a button — are all well and good, until they aren’t. If investments turn sour, shareholders tend not to be placated by being told they neglected to read the small print.

Some proposals make sense. Ditching stamp duty on UK share transactions, which is not levied on purchases of foreign shares outside the UK, is one. So are supply-side efforts such as fostering a secondary market in shares of private companies for professionals and share-owning employees.

Promoting private companies this way is a nice concept. The UK has a healthy cache of unicorns (privately held start-ups with a value of more than $1bn). CMIT cites Dealroom data that puts the UK’s stable at 138, behind only the US and China and double that of Germany, the next ranked. But unicorns can implode in clouds of fairy dust. Just ask China or consider homegrown food delivery app Deliveroo, languishing at one-third of its IPO price.

Offering incentives to invest in British companies, such as through Isas, have a patriotic community spirit ring to them. But so long as the US’s “Magnificent Seven” big tech stocks hold sway, it will take more than a few percentage points to keep investors at home.

There are some eye-watering disparities. One is the fact that in 2021 a single Canadian pension fund invested more in one UK private company than the entire UK pension industry invested across all UK private companies.

Still, an exchange, like a high street or a network, is only as good as the companies, shops or content on it.

Hydrogen starts to navigate the hype cycle

The hype cycle posits that a new technology will generate vast excitement and high expectations then bitter disappointment. From that disillusionment, a more realistic way forward may emerge.

Hydrogen, the energy source that has produced more hype than heat in recent years, is starting along that path. Electrolyser maker Thyssenkrupp Nucera sketches out the way of things to come.

The €2bn group was listed in July 2023 by Germany’s Thyssenkrupp and Italy’s De Nora, which still own three-quarters of the shares between them. Something of an oddity in an industry beset by teething problems and shrinking forecasts, it does what it says on the tin.

Its first quarter, ended in December, showed deliveries on track, a growing order book, and an increase in the number of projects that it hopes to capture. Not that it is actually making money yet. Thin margins and rising ramp-up costs contributed to operating losses, though these were widely flagged. Indeed, its results were a lone bright spot in parent Thyssenkrupp’s challenging quarter.

What makes Nucera different? The first point is that — unlike makers of smaller, flexible electrolysers — its hulking alkaline machines are designed for industrial applications such as refining and steelmaking. In its order intake, Nucera snagged contracts from Swedish producer H2 Green Steel, and from a Shell project in the Netherlands.

That is helpful. Green hydrogen’s suitability for many applications is increasingly questioned. Yet in the industrial space — whether to replace existing hydrogen production, or to provide feedstock for processes — its role is more secure.

Nucera’s second advantage, in a nascent industry, is that it is emphatically not a start-up. While its alkaline electrolyser technology is new, it is rooted in the older, chlor-alkali chemical process, which still makes up almost 40 per cent of revenues.

Similarly, while the group is newly listed, it has a pre-existing global manufacturing capacity of 1GW, out of about 8GW existing in the world. That enabled it to secure the biggest hydrogen project in the world, Saudi Arabia’s green Neom city, which accounts for more than 80 per cent of current revenues, according to Martin Wilkie at Citigroup.

Nucera’s progress has been cold comfort for investors. The stock is down by a third since the IPO as excitement drained from the wider sector. Stricter conditions to access subsidies in the US, unveiled at the end of last year, have not helped.

But, in an industry likely to be buffeted for some time to come, Nucera is at least showing what might be left once the hydrogen hype subsides.

{kind=link}