Unlock the Editor’s Digest for free

Roula Khalaf, Editor of the FT, selects her favourite stories in this weekly newsletter.

Good morning. Shares in Arm fell by a tenth in late trading yesterday after the chip designer gave slightly disappointing revenue projections for the year to come. Is this the beginning of the end of the AI stock bubble? Only if you think Arm is really an AI stock, which I don’t. Still, it tells you something about what happens when a tech stock with a high valuation comes up a little bit short. Email with better news: robert.armstrong@ft.com.

Amid prosperity, gloom

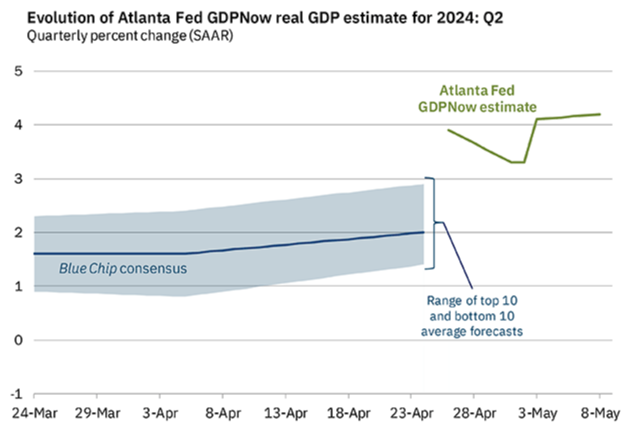

Anyone convinced that the US economy is slowing — gently or violently — owes the rest of us an explanation of this:

In the last week or so, the Atlanta Fed’s GDPNow tracker of the annual growth rate of real US output has gone from warm and falling to hot and rising. It’s still early in the quarter, and the tracker incorporates more data, becoming more accurate, as the quarter passes. But still.

It will not surprise readers of this newsletter, or of the fourth-quarter GDP report, or of most first-quarter earnings reports, that the key contributor to the hot reading is consumer spending. About two-thirds of the growth in GDPNow’s current reading derives from consumer spending; two-thirds of that comes from spending on services. Most of the growth is down to investment. Within investment, only non-residential construction is creating a drag.

But even against this robust backdrop there have been plenty of comments from economists, analysts, and money managers suggesting the economy is already cooling, or might start to soon — and that it’s not just cooling enough to get inflation to target, but enough that we should worry. I would expect this strain of commentary to persist, even if the main economic indicators continue to signal strength. The increasingly normal post-pandemic economy is still strange enough that we have no choice but to take hints of trouble seriously. This remains an environment where surprises are not surprising.

What follows, then, is a gallery of the main negative data points that I have been hearing about recently. I present them not because I think they point to a serious slowdown or even a recession, but because I think it is good to have a frank look at the liability side of the balance sheet, especially when the asset side looks as good as it does now. I will have forgotten some important ones, and I hope readers will remind me. Here goes:

-

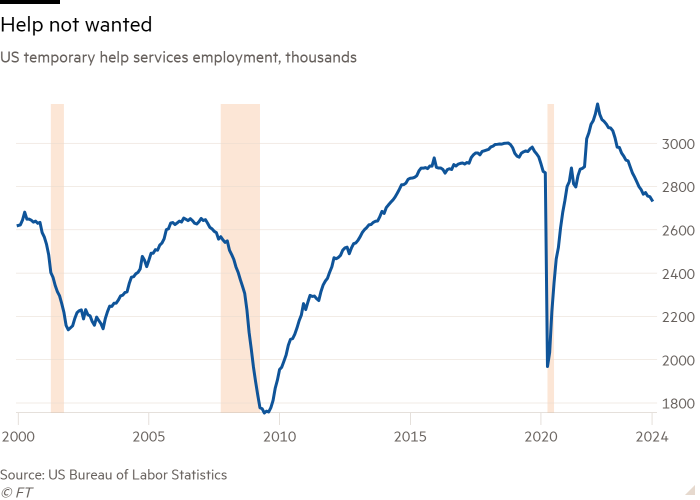

Rapid deterioration in secondary job market data. With inflation still too sticky, markets are rooting for the labour market to cool. No one wants a freeze, though. And both the quits rate and temporary employment are falling quite sharply. In normal cycles (and, again, we are not in one of those) this is a leading indicator of recession.

-

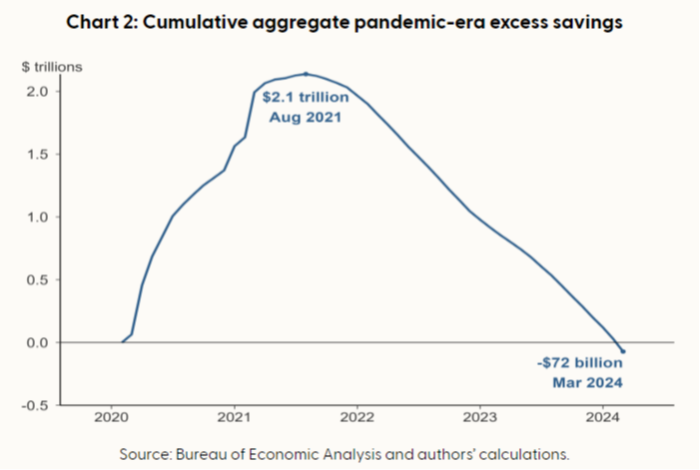

Households’ stock of pandemic excess savings is depleted, and the only thing supporting consumer spending is an unsustainably low savings rate. The savings built up while we were stuck at home collecting stimmy checks is gone, but we are all still buying loads of stuff. How long can this last? Chart from the San Francisco Fed:

-

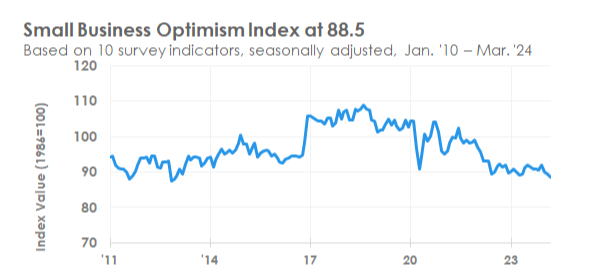

Small businesses are feeling blue. These depend on bank credit, which is expensive and hard to come by. The National Federation of Independent Business surveys say that small firms are still hiring, but less, and their profit outlook is grim. Here is the NFIB’s chart of its optimism index:

-

There is steady drumbeat of weakish anecdotes out of companies that serve the low-end consumer. “Trading down” is a familiar refrain among these companies, as we have discussed in this newsletter many times. Consumers with floating-rate liabilities and no assets to speak of have it rough right now.

-

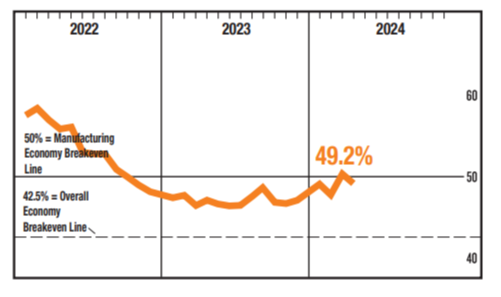

The Institute of Supply Management manufacturing survey has dropped back below 50, that is, into negative territory (the services sector trend isn’t that great, either). The previous rising trend in this indicator was a cause for relief about a sector that had been suffering. Here is the ISM’s chart:

-

Stock markets have shifted to a defensive posture. If someone had told you six weeks ago that the place to be in US stocks was utilities, you would have thought they were insane. And yet here we are. Defensives have risen and cyclicals and tech have stalled. Do stocks know something we don’t?

-

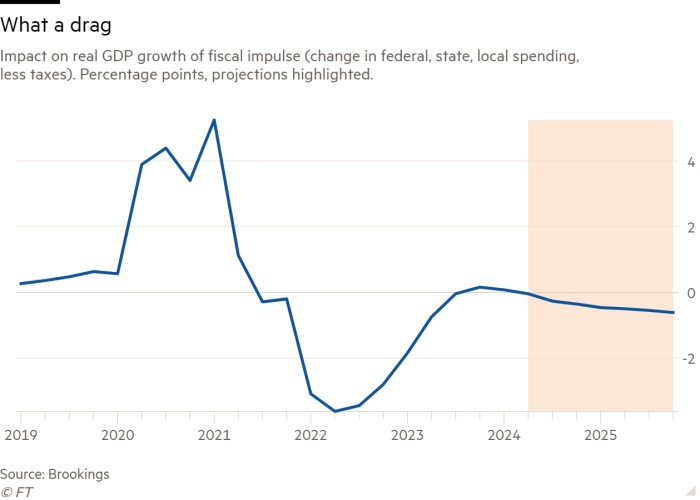

The fiscal impulse is negative. How is it possible that, with budget deficits through the roof, fiscal excess is not helping the economy? As Ethan put it a few weeks ago, the “fiscal impulse is a second-derivative measure; it tells you about changes in growth, which is itself a rate of change. It takes deficits widening to get growth to accelerate. A high but flat deficit can still put a floor under demand.” The Brookings Institution reckons that the impulse is neutral now and will be a slight drag throughout the rest of this year and next. Its chart:

-

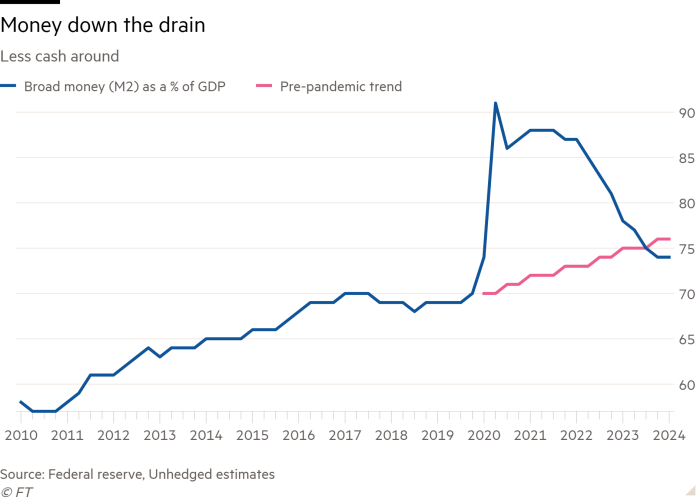

Liquidity is either flat or declining, depending how you measure it. Federal liquidity (changes in the Fed Balance sheet adjusted for changes in the Treasury general account, the Fed’s reverse repo facility, and the Bank Term Funding Program) has been going sideways for a year or so, but broad money (M2) has fallen, and is now back to its pre-pandemic trend. Yes, you have to adjust this for the velocity of money, which has risen recently. But the the pattern remains notable:

Does all of this add up to a reason to worry? My judgment is no, or at least not yet. With unemployment low, spending strong, and earnings sound, I can’t work myself up into a state of anxiety about what is next for markets. But you can be sure I will be watching these trends.

One good read

FT Unhedged podcast

Can’t get enough of Unhedged? Listen to our new podcast, for a 15-minute dive into the latest markets news and financial headlines, twice a week. Catch up on past editions of the newsletter here.

{kind=link}