It was the busiest February ever for corporate borrowers, following the busiest January ever.

Does this seem a little odd to anyone else? It’s not a shock that corporate debt markets are healthy right now — economic growth is rolling along and rates markets are no longer pricing in recession, reducing companies’ incentive for waiting — but nobody is expecting rates to rise from here. Why wouldn’t borrowers want to wait a few months?

Well, there is one big group of buyers that could be driving a short-term scramble for new corporate bonds: Life insurers.

Remember how US banks found many of their high-quality bond positions underwater after an aggressive Federal Reserve tightening cycle? Well, life insurers face their own unrealised losses on long-duration bonds after US interest rates climbed. That’s no small matter, as the entire insurance industry managed an aggregate of more than $2.8tn in bonds at the end of 2023, according to the NAIC.

A regulatory change has given life insurers an opportunity to trade out their underwater holdings of long-term corporate bonds — those hurt worst by rising US rates — for newer securities issued at higher coupons. They also have a deadline of Dec 31, 2025 to do so.

The point of the temporary accounting-rule change, from the National Association of Insurance Commissioners, was to shield life insurers’ capital from losses caused by rising interest rates.

It might sound like a niche topic, but the impact on markets could be large. In fact, life insurers could sell as much as $350bn to $400bn of long-dated corporate bond holdings and replace them with newer higher-coupon securities by the end of next year, according to estimates from Barclays strategists.

The mechanics of the NAIC’s rule change (as described by Barclays, Bank of America, regulators, industry groups and various other sources) are . . . not especially simple.

But we can start by comparing life insurers to, well, banks. (We know, we know, just bear with us.) Like banks’ held-to-maturity portfolios, life insurers don’t need to mark their bonds to market quarterly, and only report their fair value once a year.

Unlike banks, when a life insurer sells a bond, it doesn’t have to book the realised gain or loss immediately. Instead, it records its net gains (or more recently, losses) as a liability called “interest maintenance reserve” or IMR. It then smooths the gain (loss) by releasing reserves into (deducting them from) investment income over the total life of the bond — even though it doesn’t actually own that bond anymore.

IMR is also a neat way to insulate life insurers’ balance sheets from rate volatility. When an insurer sells a bond at a gain (because of falling interest rates), it has more cash on its balance sheet, which increases assets. Its liabilities increase by the same amount (through IMR), so the insurer doesn’t see a sudden jump in surplus capital.

One quirk of this rule: Insurers’ aggregated IMRs couldn’t fall below zero. So when bond sales led to a net loss, its assets would decline, but its liabilities wouldn’t. So they would deal an immediate blow to surplus capital, even as the hit to income would be smoothed over years or decades.

Of course, this accounting quirk wasn’t really a problem in Our Dearly Departed Multi-Decade Bond Bull market, when rates were falling and long-duration bonds were on a tear.

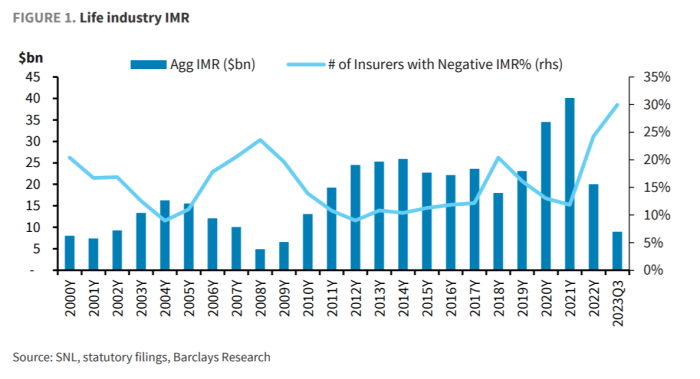

But rates are higher now. And more life insurers are sitting on net unrealised bond-trading losses (unrealised) than any time in the past 23 years, if not longer. See this chart from Barclays:

The bank estimates that roughly one-third of insurers had aggregate IMR losses as of 3Q2023. The longer-term average is 15 per cent.

That’s where the NAIC’s rule change comes in.

It allows life insurers to report negative IMRs — we love a good negative liability — to balance out the declines in cash/assets that come from selling bonds at a loss. In other words, insurers can actually take losses on underwater bonds without the immediate penalty of lower capital.

There are limits to this rule change, however. They’ll only be able to report negative IMR up to 10 per cent of their adjusted “general account capital and surplus”, assuming they can maintain enough capital relative to their risk appetite and size. (The cut-off is a risk-based capital ratio of 300 per cent, for those who are interested.)

The capital caveats make sense; presumably regulators don’t want allow life insurers to cut their asset base in half without any effect on their statutory capital surplus.

More importantly, insurers can only report negative IMR until the end of 2025. That deadline is what makes this entire situation interesting (outside of this blogger’s inexplicable interest in insurance).

For the first time in more than a decade, solid yields are available on the highest-quality bonds. The post-GFC regime of near-zero rates pushed insurers to stretch risk-taking to match liabilities, so reversing even a small portion of that shift seems reasonable.

Barclays describes the benefit to life insurers from this trade:

The relaxed regulatory rule enables life insurers to reposition their bond portfolios at a lower upfront cost than prior to the change, from a capital perspective. The change to IMR could encourage rotating from lower-coupon securities into higher ones because of the enhanced ability to defer losses. Some life insurers have already done this, based on our business interactions with the industry. To the extent this continues, it would be beneficial to future earnings given the enhancement to book yields [or the weighted average coupon of a lifer’s bond portfolio].

Life insurers could pass some or all of this benefit to policyholders through higher crediting rates, which could stimulate higher sales. In 2026, when the temporary rule expires, the benefit to capital would reverse. However, we think the incentive to increase book yields over the next two years is high enough for life insurers to accept this outcome.

So where is this trade showing up in markets? Remember, Barclays ballparked it at $300bn to $400bn. If it wasn’t obvious, this figure is way higher than the level of negative IMR that’s now allowed, because the insurers have to replace the entire principal value of the lossmaking bonds.

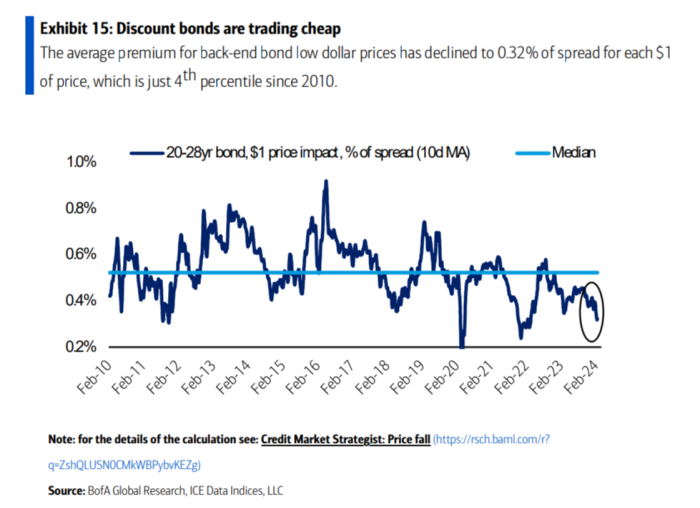

Well, life insurers should be selling bonds trading at the lowest dollar value to get the most benefit from their IMR allowances.

Indeed, low-dollar-value bonds with long maturities look very cheap compared to the past 13 years, according to BofA’s strategists (who are less convinced of the scale of insurer demand):

So there is at least some evidence to back up the idea they’re selling. And looking for signs of insurers buying brings us back to the bond-issuance boom.

The primary market is an easy (if not cheap) place to get safe bonds with high yields trading close to par, and insurers aren’t necessarily as sensitive to prices as investment managers. So presumably borrowers can get a pretty good deal from buyers, even at high-ish rates — especially if rates aren’t going to fall as far this year as many thought.

None of this really undermines the narrative of broad credit-market strength, to be sure. Bond sales are still pretty busy in the market for junk-rated bonds, where insurers are only rarely buyers. Bloomberg analysis recently had high-yield issuance on track for the busiest February since 2021.

But it does help provide some extra context for the blockbuster year for investment-grade bonds.

{kind=link}