Unlock the Editor’s Digest for free

Roula Khalaf, Editor of the FT, selects her favourite stories in this weekly newsletter.

Turns out, Donald Trump still likes tariffs. In his bid for a second term, he is promising a 10 percentage point tariff increase on all America’s trading partners, and dangling a tariff on Chinese imports of at least 60 per cent. All that might sound similar in tone to his first term, but trade watchers should quell any sense of nostalgia. His return could be quite different.

To recap, Trump’s first term started with his critics dismissing his threats as bluster. His tweets railing against bilateral trade deficits sent pundits into a frenzy, as they frothed that such figures didn’t matter. Then came the tariffs, on imported steel and aluminium, as well as hundreds of billions of dollars of imported Chinese goods. Some countries secured carve outs; others negotiated deals.

Trump’s second term would have echoes of his first. Some old disputes are still simmering: a fight over subsidies to Airbus and Boeing; a spat over digital services taxes; tension over trade in steel and aluminium. Concerns about China’s economic practices have only become more intense, as the Biden administration has maintained Trump’s tariffs and tightened restrictions on supplies of advanced chips.

But a second term would be different in at least three ways, starting with the scope of the threatened measures. During Trump’s first term, tariffs on China reshuffled activity, creating winners and losers, but with only muted macroeconomic effects. One study found that while importers bore most of the cost, retailers rather than consumers swallowed the bulk of it, limiting the effects on inflation.

Tariffs of 10 per cent on imports from everywhere and 60 per cent on goods from China would have more obvious macroeconomic effects. (They would almost certainly face legal challenges, but I’ll leave the lawyers to argue about that.)

Capital Economics, a consultancy, estimates that as an upper bound the 10 per cent tariff could lift inflation to between 3 and 4 per cent by the end of 2025. Bigger exchange rate movements seem likely. And retaliation seems inevitable, particularly now the European Commission has new powers to hit back outside of the World Trade Organization’s hobbled system of solving disputes.

A second difference would be in the nature of the debate. Screeching about America’s bilateral trade deficit with China can now be informed by the experience of the first batch of tariffs. That reduced the bilateral trade deficit with China by a bit, but was more than offset by increasing trade deficits with other countries including Mexico, some of which are closely tied to China’s supply chains.

The discussion around a 10 per cent tariff should be more interesting, though controversial. Former US trade representative Robert Lighthizer, who seems likely to serve in the next administration, has argued that America’s problem is not necessarily bilateral trade deficits (absent unfair practices), nor even a trade deficit in any single year. Rather, a broader import tax is supposed to tackle America’s pattern of consistent trade deficits, year after year.

A third difference between Trump’s first and second term reflects the evolving position of China. On top of the cemented concerns about China’s chip production, the Biden administration recently issued a public warning for it not to solve its domestic economic weakness by pumping out manufactured goods to sell overseas.

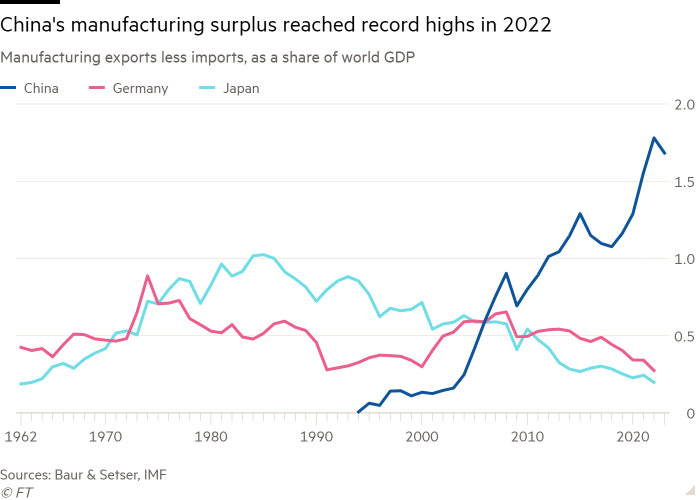

A glance at official data suggests that China’s current account surplus isn’t much different from 2016. But Brad Setser of the Council on Foreign Relations says there is something fishy about the figures. Other indicators suggest sharply rising Chinese manufacturing exports. Setser’s work with Volkmar Baur of Union Investment, an asset manager, suggests that in 2022 China’s surplus in manufacturing goods grew to record highs, of almost 2 per cent of world gross domestic product.

During Trump’s first term the European Commission did not apply broad measures to deter the trade diverted from America, beyond those on steel. And between 2018 and 2020, the trend in its aggregate imports from China did not obviously change. But since the pandemic, the EU’s trade deficit with China has risen sharply, to the point of becoming a source of political tension.

If Trump follows through with new restrictions on America’s trading partners in general and China in particular, the pressure on European producers would grow. Their access to the US market would be restricted. And they would also face stiffer competition in other markets, including their own, due to other trade being diverted away from America. In that context, it seems easier to imagine Trump’s taste for tariffs catching on.

{kind=link}