Good morning. Berkshire Hathaway was a net seller of equities (including Apple shares) in the first quarter and its cash pile grew to a new record. It is hard not to conclude that the high returns available on short-term Treasuries are making its mark on the Berkshire portfolio, despite Warren Buffett’s insistence that cash yields don’t matter (“We don’t use the cash now at 5.4 per cent but we wouldn’t use it if it was at 1 per cent . . . we only swing at pitches we like.”). Let me know your thoughts: robert.armstrong@ft.com.

How good was that jobs report?

Until last Friday, the evidence that the economy was slowing and bringing inflation down with it consisted of smallish data items and anecdotal corporate testimony. A slightly weaker ISM or consumer confidence reading here; bad news from McDonald’s and Starbucks there. Friday’s weaker-than-expected jobs report — 175,000 jobs added, against an expected 241,000 — represents a meaty, important data point around which all those other bits and bobs can coalesce.

In the chart below, the light blue line shows why the news was welcomed so warmly by markets. What looked very much like a re-accelerating trend in job creation over the previous four months is suddenly more ambiguous:

Still, the three- and six-months averages, which remain sideways-to-up, remind us that April is just one month. Happily, the wage data is more encouraging still. A quite clear, multi-month cooling trend is in place:

Over at The Overshoot, Matt Klein looks at the evidence and concludes that “US inflation may be much closer to normalisation than I had previously thought.” Wage growth and inflation are closely linked, Klein notes, for the simple reason that consumer spending is mostly funded by wages and most business revenue is funded, directly or indirectly, by consumer spending. We have now had three consecutive months in which the nominal wage data, considered in its totality, has been below the high trend that began back in mid-2022:

Aggregate weekly wage income, which is average hourly pay multiplied by the number of people on payrolls times the number of hours worked each week . . . translates pretty closely to nominal gross domestic product, and was unchanged in April 2024 . . . That would make last month the weakest month for aggregate nominal income growth since February 2021

Unhedged has taken the view that the patchy evidence of a slowdown and cooling inflation is outweighed by other evidence suggesting above-trend growth and still-warm inflation. With this jobs report, we’re edging — provisionally — towards the idea that a slowdown might be beginning. That suggests there may be rate cuts in 2024 after all, an outcome markets would welcome.

That said, it may be that the sticky inflation we are seeing now is about more than consumers’ ability and willingness to spend. Structural or supply-side factors may be more important. If so, while it may be that (as Klein has argued) wage growth below a certain threshold is necessary for inflation getting to target, it is not sufficient.

Two pieces in the FT over the weekend make this point in slightly different ways.

Mohamed El-Erian approves of the Fed’s decision to all but rule out further rate increases, but not because the current stance of policy is tight enough to bring inflation down to the two per cent target eventually. Instead, he thinks getting to that target would do pointless damage to the economy, which is more inflationary than previously for structural reasons:

Economic developments are likely to show that the Fed is unable to get to 2 per cent unless it is willing to impose large and unnecessary damage on the economy. Indeed, 2 per cent may not be the right inflation target for an economy going through so many structural changes, both domestically and internationally . . . multiyear structural transitions that are inherently inflationary. Domestically, the US has been moving away from deregulation, liberalisation and fiscal prudence to tighter regulation, industrial policy and chronic fiscal looseness.

Tej Parikh argues that the economy is now less rate sensitive, both because of the terming out of consumer and corporate debt, and because of the less capital-intensive, more service intensive nature of modern business. Increasing rates aggressively hits only select parts of the economy, such as construction, transportation, and poorer households. Meanwhile, the main causes of sticky inflation go largely untouched:

Today, America’s sticky CPI holdouts are shelter and motor vehicle insurance. Both are partly a product of pandemic supply shocks — reduced construction and a shortage of vehicle parts — that are still percolating through the supply chain. Indeed, dearer car insurance now is a product of past cost pressures in vehicles. Demand is not the central problem

Both El-Erian and Parikh are counselling against the Fed pushing too hard on rates to get inflation all the way to target, because the costs might not be worth the benefits. But there is another lesson in what they argue. Part of the “last mile” inflation problem is only partly to do with excess demand, so a softer jobs market might not be enough to solve it.

Utilities and the sector-performance flip

A month ago I wrote that, in the equity rally reaching back to October of 2022, Utilities were far and away the worst performing sector. I showed a chart that looked a lot like this one:

I wrote then that

If you believe that, sooner or later, markets revert towards the mean, utilities are setting up for an absolutely glorious reversion. And this has happened in the past: in 2011 and 2014, for example, after several years of underperformance, utilities’ returns roared back and crushed the market by 15 and 18 percentage points, respectively. Utility outperformance is not limited to recessions and big market corrections.

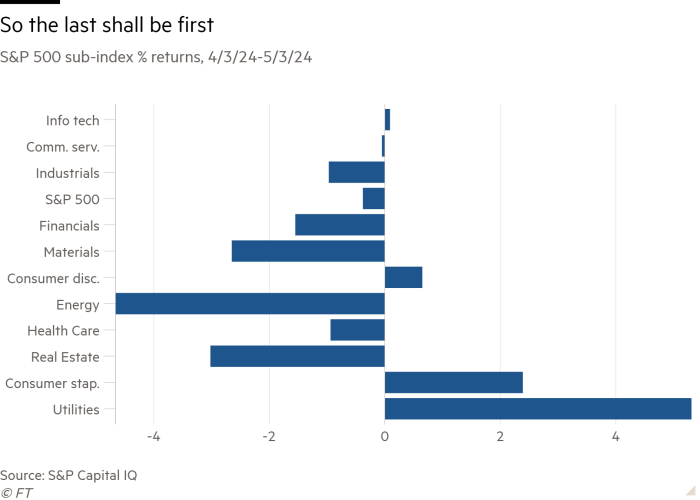

Well, here is what has happened in the month since:

Not only utilities, but their fellow defensive sector consumer staples, have gone from being the worst to the best performers. Cyclicals such as financial and industrials, on the other hand, went from leading the way (trailing only the sectors dominated by big tech) to badly lagging the market.

I mention this not as evidence that I can predict when mean reversion is going to happen. My history as an investor proves conclusively that I cannot. Instead, the point here is that the market has not simply lost momentum since the rally came to a halt in April. Its internal dynamic has shifted as well and this shift is not simply down to changing rate expectations. Utilities, as sometime bond substitutes, are usually rate sensitive. The prospect of higher-for-longer rates should hurt them, all else equal (it certainly did in much of 2023 and early 2024). But investors in US equities appear be putting a big premium on safety, all of a sudden, and looking part utilities relative yields

Nicholas Bohnsack of Strategas, upgrading the utility sector this week, noted that its valuation is low relative to their own recent history and the rest of the S&P 500, despite solid earnings growth expectations for this year. I myself don’t know whether utilities’ strong relative performance will continue, but it does seem to suggest a change in investor risk appetite, perhaps in response to the (still patchy) evidence that the economy is slowing.

One good read

The restless hunt for dullness.

FT Unhedged podcast

Can’t get enough of Unhedged? Listen to our new podcast, for a 15-minute dive into the latest markets news and financial headlines, twice a week. Catch up on past editions of the newsletter here.

{kind=link}