Every year the markets provide us with lessons on prudent investment strategies. And with great frequency, markets offer remedial courses covering lessons they previously taught.

That’s why one of my favorite sayings is that there’s nothing new in investing, only investment history you don’t know. In 2023, investors were provided with 12 lessons. Many of them are repeats from prior years. Unfortunately, too many investors fail to learn them.

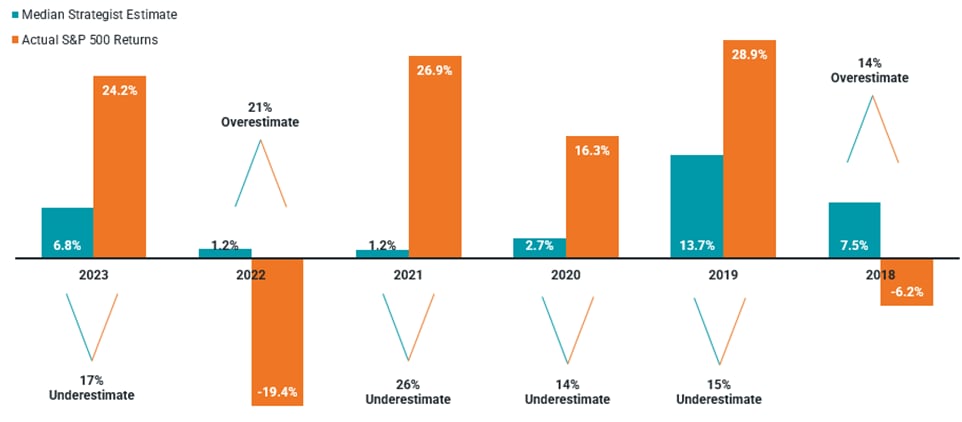

Lesson 1: No One is Very Good at Market Forecasts

The only value in market strategist forecasts is they show that a wide dispersion of outcomes is possible. The S&P 500 ended 2022 at 3,839.50. The forecasts of 23 analysts from leading investment firms for year-end 2023 ranged from as low as 3,650 (down 5%) to as high as 4,750 (up 24%). The average forecast was for the S&P 500 to end the year at 4,080 (up 6%). It closed the year up 26.4%.

The following chart from Avantis shows that not only is such a wide dispersion of potential outcomes likely, but the median forecast is typically wrong by a wide margin.

Consensus S&P 500 Estimates vs. Actual Returns (2018-2023)

The lesson is that investors are best served by following Warren Buffett’s advice on guru forecasts: “We have long felt that the only value of stock forecasters is to make fortunetellers look good. Even now, Charlie [Munger] and I continue to believe that short-term market forecasts are poison and should be kept locked up in a safe place, away from children and also from grown-ups who behave in the market like children.”

The lesson is an especially important one because investors, like all humans, are subject to confirmation bias. Thus, when we hear a forecast that confirms our own beliefs or concerns, we are more likely to act on it than if we hear a contrary opinion.

Lesson 2: The ‘Magnificent 7’ is a Bit Misleading

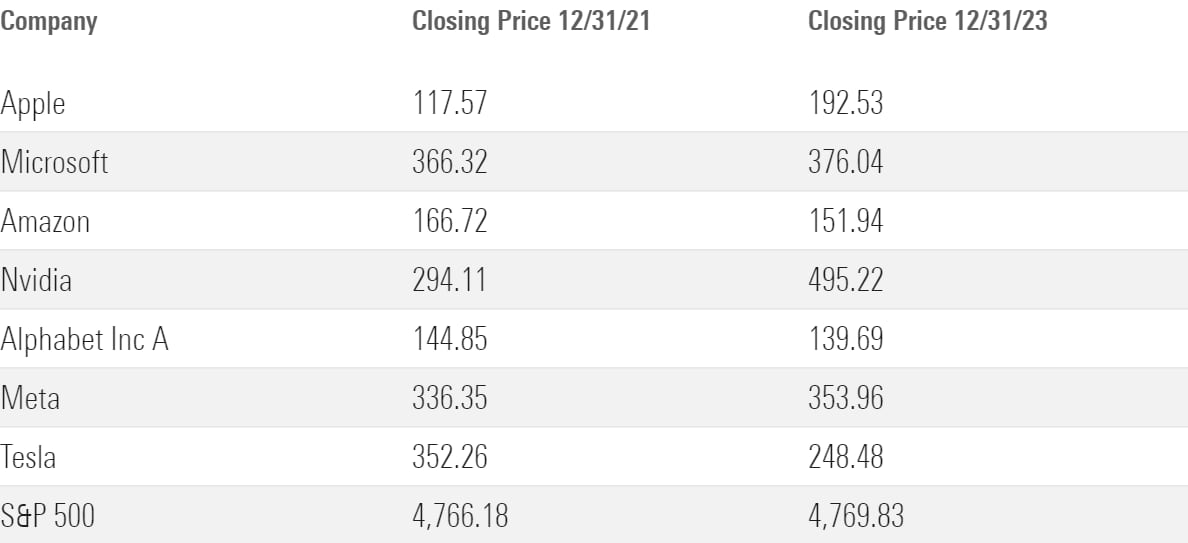

Three of the “Magnificent Seven” companies (Tesla [TSLA], Alphabet [GOOGL], and Amazon.com [AMZN]) ended 2023 below their closing price at the end of 2021.

Only three (Apple [AAPL], Microsoft [MSFT], and Nvidia [NVDA]) outperformed riskless one-month Treasury bills, which returned 3.2% per year over the period.

Magnificent Seven Stocks 2021 and 2023 Closing Prices

While the S&P 500’s return for 2023 was 26.4%, the performance of the Magnificent Seven was responsible for most of the returns, as their average total return was 104.7%, accounting for more than 62% of the S&P 500’s performance.

That performance was greatly affected by investor fascination with the “AI story.” But history provides cautionary warnings about sky-high valuations driven by stories. A recent example is that Lidar (autonomous vehicle technology) stocks have collapsed by 85% from their peak. The valuations of the Magnificent Seven, with an average price-to-earnings of 50, are now reminiscent of the high valuations of the Nifty 50 and the dot-com stocks just before crashing. While not a forecast of a crash, it is a warning that at the very least these stocks, which currently make up about 30% of the total market cap of the S&P 500, are at historically extreme valuations. Fortunately, the rest of the market has valuations that are much closer to their historical averages.

The lesson is that it is very difficult for highly valued companies to continue to outperform over the long term. The reason is that the empirical evidence demonstrates that abnormally high growth in earnings tends to revert to the mean at a rate of about 40%, and real-world forecasts tend to underestimate the speed at which reversion to the mean in profitability occurs. Another lesson is that while story stocks may be fascinating, they typically don’t make for great investments.

Lesson 3: Don’t Use Valuations to Time Markets

We entered 2021 with equity valuations at a high.

In particular, the popular metric known as the Shiller Cyclically Adjusted PE Ratio 10 – a measure of price to earnings based on real-per share earnings over a ten-year period – was about 34 for US stocks, well above the historical average of about 17. We had been above that just one other time (in the late 1990s) and that was followed by a severe bear market.

That led many forecasters to predict poor returns. For example, “legendary” investor Jeremy Grantham, long-term investment strategist at GMO, predicted 2021 would see a stock market crash: “when the decline comes, it will perhaps be bigger and better than anything previously in US history,” he has said. Investors who listened to that advice and sold equities missed out on the market’s strong performance that year. Vanguard S&P 500 ETF VOO returned 28.8%!

That strong performance drove the CAPE 10 to 38.3, even higher than its historical average. In 2022, the S&P 500 performed poorly, losing 18.1%. But that loss still left the CAPE 10 at 28.3, again leading many to predict a year of poor performance. Defying such forecasts, the S&P 500 returned 26.4% in 2023.

While valuations provide valuable information about future expected returns over the long term (there’s about a 0.4 correlation between the two over 10-year periods), that doesn’t mean you can use that information to time markets. The evidence shows such efforts are likely to fail.

This doesn’t mean, however, that the information has no value. You should use valuations to provide estimates of returns so you can determine how much equity risk you need to take in your portfolio to have a good chance of achieving your financial goals. But expected returns should be treated only as the mean of a potentially wide dispersion of outcomes. Your plan should address any of these outcomes, good or bad.

Lesson 4: it Takes Discipline to Stay the Course

All strategies that entail investing in risk assets are virtually guaranteed to experience long periods of underperformance. If you doubt that, consider that the S&P 500 has experienced three periods of at least 13 years when it underperformed riskless one-month Treasury bills (1929-43, 1966-82, and 2000-12). To gain the benefits of diversifying away from traditional 60/40 portfolios, you must have the discipline to stay the course (and even rebalance) during periods of negative performance.

Lesson 5: Assets Have Self-Healing Mechanisms

When risk assets have poor returns, it is usually attributable to a combination of poor performance (falling earnings or producing losses) and falling valuations. Because the best predictor we have of future equity returns is the earnings yield (the inverse of the P/E ratio, or E/P), falling valuations mean that future expected returns are now higher. Investors subject to recency bias fail to understand that, leading them to sell instead of buying.

Falling valuations are a “self-healing” mechanism. For example, after underperforming one-month Treasury bills from 2000 through 2012, the CAPE 10 had fallen to 21.2 from 44.2.

From 2013 through 2021, the S&P 500 returned 12.6% per year, outperforming one-month Treasury bills by 11 percentage points per year. Similarly, the S&P’s loss of 18.1% in 2022 resulted in the CAPE 10 falling to 28.3 from 38.3.

The lesson for investors is to remember self-healing mechanisms are at work after periods of poor performance. Sophisticated investors know that the winning strategy is to avoid being subject to recency bias and to follow Warren Buffett’s advice to avoid market timing, but if you cannot resist “be fearful when others are greedy and be greedy only when others are fearful.”

Lesson 6: Even With a Crystal Ball, Markets Are Wild

Imagine that on January 1 2023, you were provided with a crystal ball that would enable you to see the major geopolitical and economic events of the coming year.

Given what happened, it’s hard to imagine any investor would have predicted that the S&P 500 would rise 26.4%. And it is likely that many investors would have sold equities given the negative news that was coming.

The lesson is that even if you could accurately predict events, you should not try to time markets based on forecasts.

Lesson 7: Don’t Let Politics Influence Decisions

One of my more important roles as head of financial and economic research at Buckingham Wealth Partners is helping to prevent investors from committing “portfolio suicide”: panicked selling resulting from fear, whatever its source, including the political arena.

We often make mistakes because we are unaware that our decisions are being influenced by our beliefs and biases. The first step to eliminating, or at least minimising, such mistakes is to become aware of how our choices are affected by our views, and how those views can influence outcomes. The 2012 study Political Climate, Optimism, and Investment Decisions by Yosef Bonaparte, Alok Kumar, and Jeremy Page, showed that people’s optimism toward both the financial markets and the economy is dynamically influenced by their political affiliation and the existing political climate.

Now, imagine the nervous investor (and I have had discussions with many of them, all of whom were Republicans) who reduced their allocation to equities (or even eliminated them) based on views about the Joe Biden presidency, Democratic control of the Senate, and the exploding budget deficits (among other concerns).

While investors who stayed disciplined benefited from the market’s very strong performance, those who panicked and sold not only missed out on that strong performance but persistently faced (and continue to face) the incredibly difficult task of figuring out when it would be safe to invest again. Similarly, I know of many investors with Democratic leanings who were underinvested after President Donald Trump was elected.

The lesson to ignore your political views when making investment decisions is one that rears its head after every presidential election. The election of 2024 will be no exception. Remember to express your views with your votes, not with your investments. Forewarned is forearmed.

Lesson 8: Most Returns Were Earned in Short Periods

Over the first 10 months of 2023, small caps performed poorly. For example, Vanguard Russell 2000 ETF (VTWO) produced a return of negative 4.4% and Avantis Small Value ETF AVUV returned just 0.8%. Both far underperformed (VOO), which returned 10.6%.

Impatient, undisciplined investors and those subject to recency bias may have abandoned their investments in small and small-value stocks. Over the next two months, VOO returned 14.2%, VTWO returned 22.4%, and AVUV returned 21.9%.

The historical evidence demonstrates that this is the norm. For example, over the 97-year period from 1927 through 2023, the S&P 500 returned 10.3% annualised. If we were to remove the returns of the highest-returning 97 months, what would you guess was the return of the remaining 1,067 months?

Most investors would be shocked to learn that the answer is virtually zero. The remaining 1,067 months provided an average annual return of just 0.01%. The best 97 months (just 8.3% of the months) provided an average annual return of 10.4% – more than 100% of the annualised return over the full period!

The lesson for investors is that the ability to avoid the temptation to chase recent performance is a necessary ingredient for investment success.

Lesson 9: 2023’s Winners Might be This Year’s Dogs

The historical evidence demonstrates that individual investors are performance-chasers – they buy yesterday’s winners (after the great performance) and sell yesterday’s losers (after the loss has already been incurred). This causes investors to buy high and sell low – not a recipe for investment success.

As I wrote in my book The Quest for Alpha that behaviour explains the findings from studies that show investors can underperform the very mutual funds they invest in. Unfortunately, a good (or poor) return in one year doesn’t predict a good (or poor) return in the next. In fact, great returns lower future expected returns, and below-average returns raise future expected returns.

Lesson 10: Active Management is a Loser’s Game

Last year was another in which most active funds underperformed even though the industry claims that active managers outperform in bear markets. In addition to the advantage of being able to go to cash, active managers had a great opportunity to generate alpha through the large dispersion in returns between 2023’s best-performing and worst-performing stocks. For example, while the S&P 500 returned 26.4% for the year, including dividends, in terms of price-only returns, the stocks of 10 companies were up at least 64.9%.

To outperform, all an active manager had to do was overweight those big winners. On the other hand, 10 stocks lost at least 32.4% (underperforming the S&P 500 by almost 59 percentage points). To outperform, all an active manager had to do was underweight or avoid these dogs.

This wide dispersion of returns is not at all unusual. Yet, despite the opportunity, year after year in aggregate, active managers persistently fail to outperform.

Lesson 11: Diversification is Always Working

Everyone is familiar with the benefits of diversification.

Done properly, it reduces risk without reducing expected returns. But once you diversify beyond a popular index such as the S&P 500, you must accept the fact you will almost certainly be faced with periods (even long ones) when a popular benchmark index, reported by the media daily, outperforms your more diversified portfolio. The noise of the media will then test your ability to adhere to your strategy.

Of course, no one ever complains when their diversified portfolio experiences positive tracking variance (that is, it outperforms the popular benchmark). The only time you hear complaints is when it experiences negative tracking variance (that is, it underperforms the benchmark). Successful investing requires the discipline and patience to keep you from abandoning your long-term plan.

Lesson 12: Innovations Are Not Always Investments

The year 2023 witnessed the fall of several companies that were once heralded as pioneers of innovation. WeWork declared bankruptcy in November. It was valued in 2019 at $47 billion in a round led by Masayoshi Son’s Softbank (SFTBY). It eventually went public in 2021, with a valuation of $9.4 billion via a special-purpose acquisition company.

Bird, an electric scooter company that was heralded as a vanguard in the new “sharing” economy and was valued at $2.5 billion in 2019, declared bankruptcy in December. Even Instant Brands, the firm behind a cultural kitchen phenomenon (and the maker of Instant Pot), filed for bankruptcy. Their innovations were not enough to immunise them against economic slumps, slowing sales, management missteps, and myriad other issues that caused their demise and the ultimate destruction of immense shareholder value.

The views expressed here are the author’s. Larry Swedroe is head of financial and economic research for Buckingham Wealth Partners, collectively Buckingham Strategic Wealth, LLC and Buckingham Strategic Partners, LLC.

For informational and educational purposes only and should not be construed as specific investment, accounting, legal, or tax advice. Certain information is based on third-party data and may become outdated or otherwise superseded without notice. Information from sources deemed reliable, but its accuracy and completeness cannot be guaranteed.

Investors should carefully consider any fund investment risks and investment objectives. Certain funds may not be appropriate for all investors and are not designed to be a completed investment program. As such, this article does not constitute a recommendation to purchase a specific security and it should not be assumed that the securities referenced herein were or will prove to be profitable. No strategy assures success or protects against loss.

Performance is historical and does not guarantee future results. All investments involve risk, including loss of principal. Individuals should speak with their qualified financial professional based on their own circumstances to discuss the ideas presented in this article.

{kind=link}